Authors: Rosie Davenport & Esther Val

While other global powerhouses continue to be hauled over the coals for their climate policy inertia, the European Union has emerged with bold aspirations to lead the international sustainability agenda. The implications of its ambitions are already being felt across EU and non-EU companies who trade in the bloc. The EU’s Green Deal policy agenda and its Fit for 55 package sets out a swathe of interconnected proposals with legislative and compliance obligations impacting every sector.

Europe’s aim to become the global leader on sustainability has far-reaching implications for EU and non-EU companies doing business in the bloc. European banks and investors, as well as leading companies at the top of value chains, are rapidly realigning their strategies to comply with the current and emerging regulation set out under the umbrella of the EU Green Deal. Since the majority of their clients and suppliers are SMEs, it is important that they understand the implications and adapt their business models accordingly. And, even in the post-Brexit world of non-regulatory alignment, it’s widely acknowledged that the EU Green Deal’s policies will inevitably affect Britain’s markets, trade negotiations and stance on global climate action. In fact, 63% of UK asset management firms are already implementing the EU’s taxonomy regulation, according to a recent PwC survey.

The EU’s Green Deal also places significant new responsibilities on SMEs. Representing 99% of all EU businesses and accounting for over 50% of Europe’s GDP,SMEs are instrumental to the Green Deal’s success. While SMEs are capable of bringing significant innovations to address climate change and energy efficient business practices, it’s vital they aren’t swamped with burdensome regulation. As a 2019 Business Survey by Eurochambres shows, red tape already represents a major challenge to 78% of SMEs. This figure underscores the need for clear guidance to be given to SMEs to improve their ability to contribute to the green transition.

So what do SMEs need to know to get ahead of the legislative curve? Here’s our overview of the current EU Green Deal’s climate change/sustainability policy framework along with support and funding opportunities that could smooth your transition. We also take a look at the ever increasing regulatory changes in the pipeline that SMEs need to be aware of in order to reap all the benefits of the green transition.

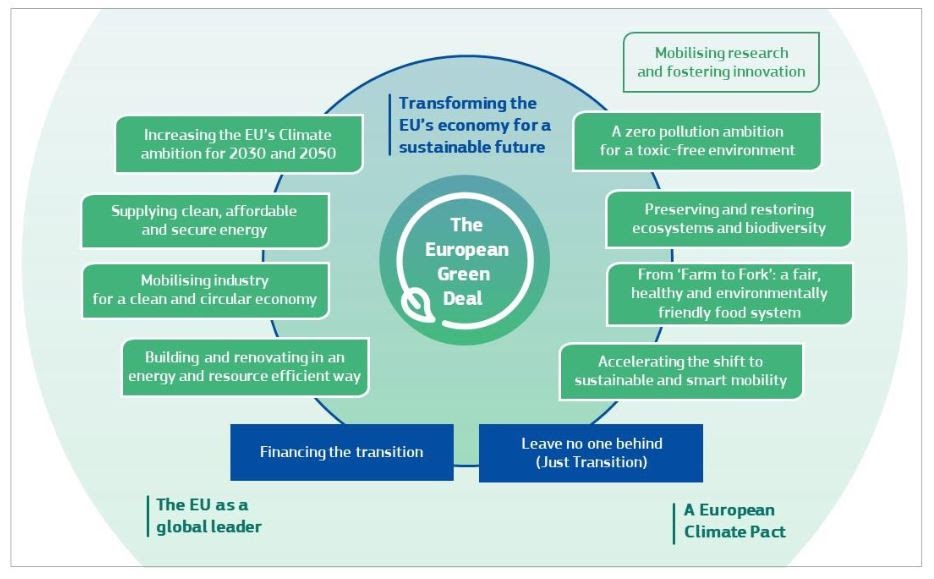

What is the EU Green Deal?

In December 2019, the European Commission announced the European Green Deal – the EU’s strategy to achieve the UN Sustainable Development Goals and the Paris Agreement – and its ambition to become the world’s first ‘climate-neutral bloc’ by 2050.

Source: European Commission.

{kind=link}

It includes a range of ambitious environmental policies as well as comprehensive plans for industrial policies, digitalisation, financing mechanisms and investment programmes. The EU’s strategy is underpinned by a massive investment plan – worth €1 trillion over the next 10 years. As part of the Green Deal, a new Circular Economy Action Plan will introduce targets and regulations on a range of products to ensure that ‘by 2030, only safer, circular and sustainable products should be placed on the EU market’. This will have clear implications for non-EU companies wanting to trade with the largest economy in the world.

Fit for 55

In order to implement the Green Deal, on 14 July 2021, the European Commission adopted a number of legislative proposals setting out how it intends to achieve climate neutrality in the EU by 2050, including the intermediate target of an at least 55% net reduction in greenhouse gas emissions by 2030.

Why is it important for SMEs?

- Fit for 55 brings business policy certainty and clarity to support the deep transformations needed to deliver the EU’s climate targets

- It sets out a framework to increase investor certainty

- It allocates financial resources to fund SMEs’ climate transition, including the following initiatives

- At least 37% of the NextGenerationEU fund has been earmarked at to support business’ green transition.

- 30% of programmes under the 2021-2027 Multiannual Financial Framework are dedicated to support climate action (for example the LIFE programme)

- The Innovation Fund will support business and SMEs’ investment in clean energy

- 35% of research and innovation funding under Horizon Europe will be allocated to green investments as well as various partnerships and ‘mission’ activities.

EU Taxonomy

In order to meet the EU Green Deal’s aims, investment needs to be channeled towards sustainable projects and activities. To achieve this, the EU is currently developing an EU Taxonomy, a science-based classification system set to become the global standard, to determine whether an investment-seeking business activity is environmentally sustainable. The Taxonomy is likely to become the global standard and is expected to shift investments toward a low-carbon, climate-resilient economy, helping companies be more sustainably minded while protecting private investors from greenwashing.

Although the Taxonomy is a European regulation, it will have implications for foreign markets that conduct business with Europe. Conversely, European companies operating globally are likely to apply the EU Taxonomy lens to their global operations.

To illustrate that point, an expert advisory committee convened by the City of London’s Green Finance Institute is currently working on a Taxonomy. The UK Government has said it will be broadly in line with the EU Taxonomy.

The Taxonomy sets out that economic activities should ‘substantially contribute’ to at least one of six environmental objectives, ‘do no significant harm’ to any of the other five environmental objectives, and comply with ‘minimum social safeguards’.

Why is it important for SMEs?

- European institutional investors and asset managers will have an obligation to disclose how their sustainable fund aligns to the EU Taxonomy. So investment targets, including SMEs, will have to demonstrate how aligned their business is to the Taxonomy.

- To reduce regulatory and financial risk from a lack of future investment and also highlight opportunities, SMEs will need to adapt their business practices not aligned with the Taxonomy

Timetable

The EU Taxonomy framework is being phased in, with level one coming into force in July 2020. On 21 April 2021 the Commission adopted its level 2 legislation, or “delegated acts,” defining the technical screening criteria for the first two objectives: climate change mitigation and adaptation. Investors will officially need to start reporting on the environmental, social and governance (ESG) alignment of their funding, based on the Taxonomy framework, by 1st January, 2022, covering the reporting period of 2021.

The criteria for other environmental objectives is expected to be published shortly.

Corporate Sustainability Reporting Directive (CSRD)

Until now, SMEs have largely been exempt from sustainability reporting. Under the Non-financial Reporting Directive (NFRD), only companies with over 500 employees were required to disclose non-financial information. However, this will change as the NFRD is being revised to include listed SMEs, with the exception of listed micro-enterprises.

The new rules mean nearly 50,000 companies across the EU will now have to report on sustainability in line with guidelines currently in development.

Companies will be legally required to report if they meet two of the following three criteria:

1) 250+ employees;

2) €40 million+ turnover; and/or

3) €20 million+ total assets.

On 8th July 2021, the European Financial Reporting Advisory Group (EFRAG), the EU body in charge of developing the EU reporting standards, announced it will be building on the GRI framework to develop the final guidelines. The GRI Standards are currently the most commonly used sustainability reporting framework amongst EU companies.

The new disclosure requirements will include:

-information about strategy, targets, the role of the board and senior management, the key adverse impacts connected to the company and its value chain, and intangibles (i.e. social, human and intellectual capital).

-information on risks to companies but also the impacts of companies on society and the environment (the so-called ‘double materiality’ principle).

-extent of alignment with the EU Taxonomy.

SMEs in scope will be allowed to report according to a simplified standard while non-listed SMEs are encouraged to report on a voluntary basis to anticipate regulatory, market trends and stakeholder demands.

Why is it important for SMEs?

- SMEs are already facing growing requests for sustainability information from banks that lend them money and large companies that they supply. They need the information partly to meet their own disclosure requirements under the Sustainable Finance Disclosure Regulation.

- Without relevant sustainability reporting, SMEs will increasingly find themselves at a competitive disadvantage, missing new market opportunities, and being prevented from accessing resources for development of new technological solutions. As an indication of the prize they could miss out on, he EU plans to mobilise €1 billion public investments annually to fund new technologies.

{kind=link}

Timetable

Adoption of the new reporting directive is expected by the first half of 2022. The Commission would then publish the first set of reporting standards by the end of 2022. Large companies will apply the standards to reports published in 2024, covering the 2023 financial year.

However, there is a three-year delay for SMEs to apply the new reporting rules.

What do SMEs need to do now?

- Understand the implications of the new policy/regulation framework and the sustainability-related demands from regulators, investors, consumers and other stakeholders.

- Formulate a sustainability strategy and a roadmap with actions needed to comply with new regulations.

- Set metrics and put processes in place to capture data and measure progress

- Identify material topics in consultation with stakeholders.

- Start the process of reporting your material topics, sustainability strategy and actions referencing GRI standards

- Take stock of lessons learned and aim to improve your reporting standards every year following feedback from stakeholders

References:

https://ec.europa.eu/commission/presscorner/detail/en/QANDA_21_1806

https://www.greenbiz.com/article/what-you-should-know-about-eu-taxonomy

https://ec.europa.eu/growth/smes_en

https://www.esginvestor.net/smes-and-the-future-of-european-sustainability-reporting-rules/

https://ec.europa.eu/info/sites/default/files/communication-sme-strategy-march-2020_en.pdf

https://www.chathamhouse.org/2020/02/what-european-green-deal-means-uk

https://futureofsustainabledata.com/taxomania/

Cover photo by Nick Morrison on Unsplash